Satisficing and optimizing

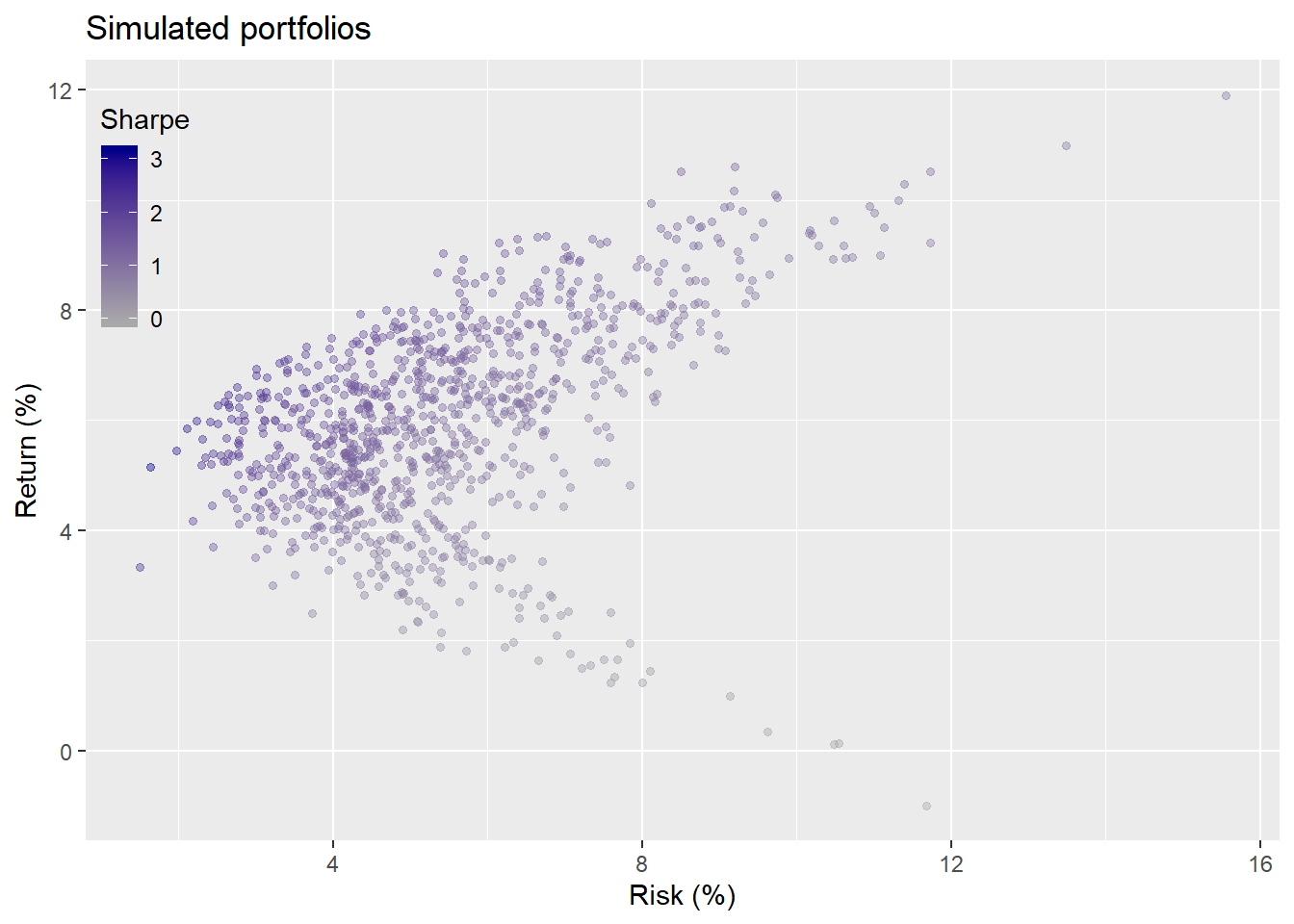

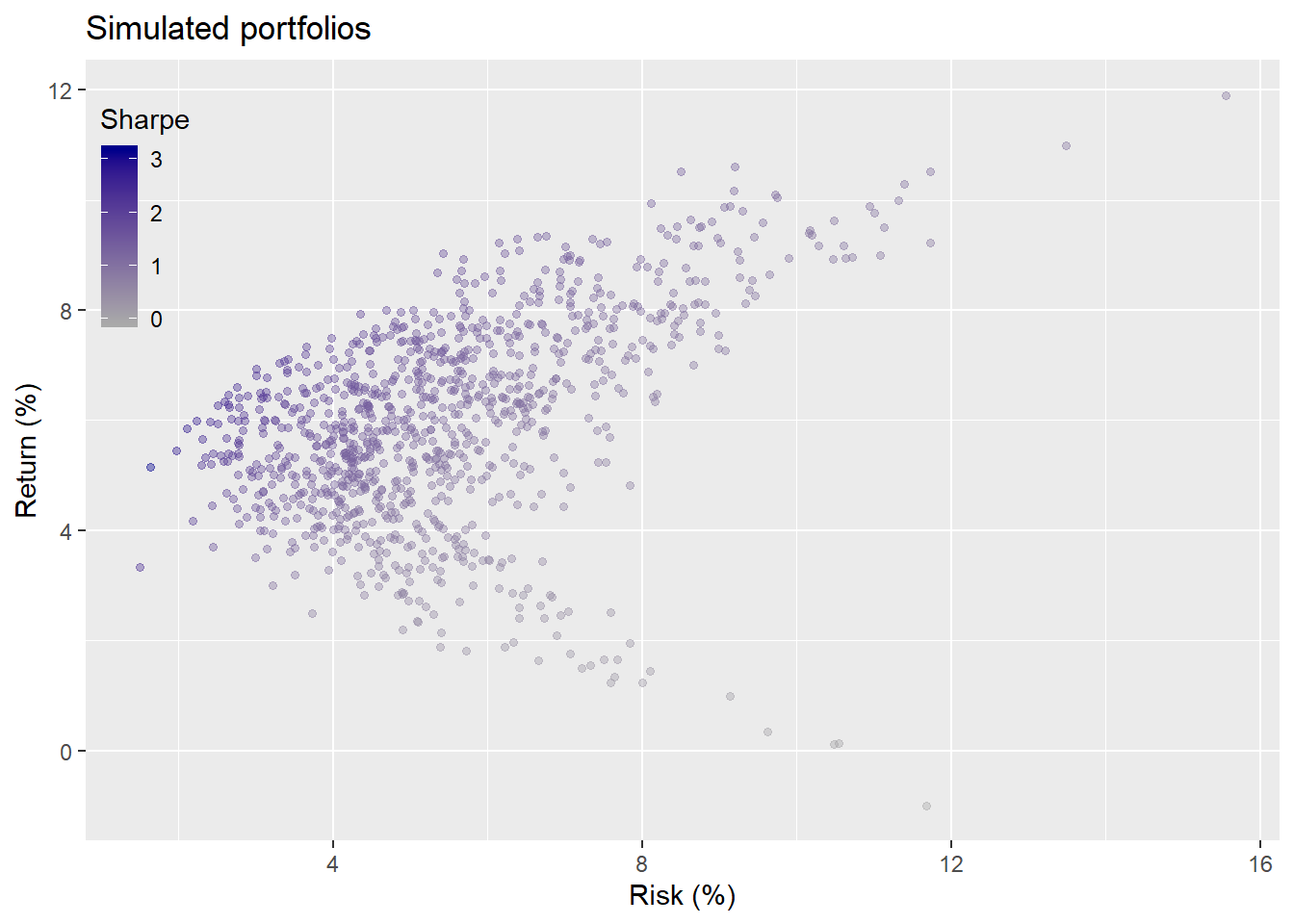

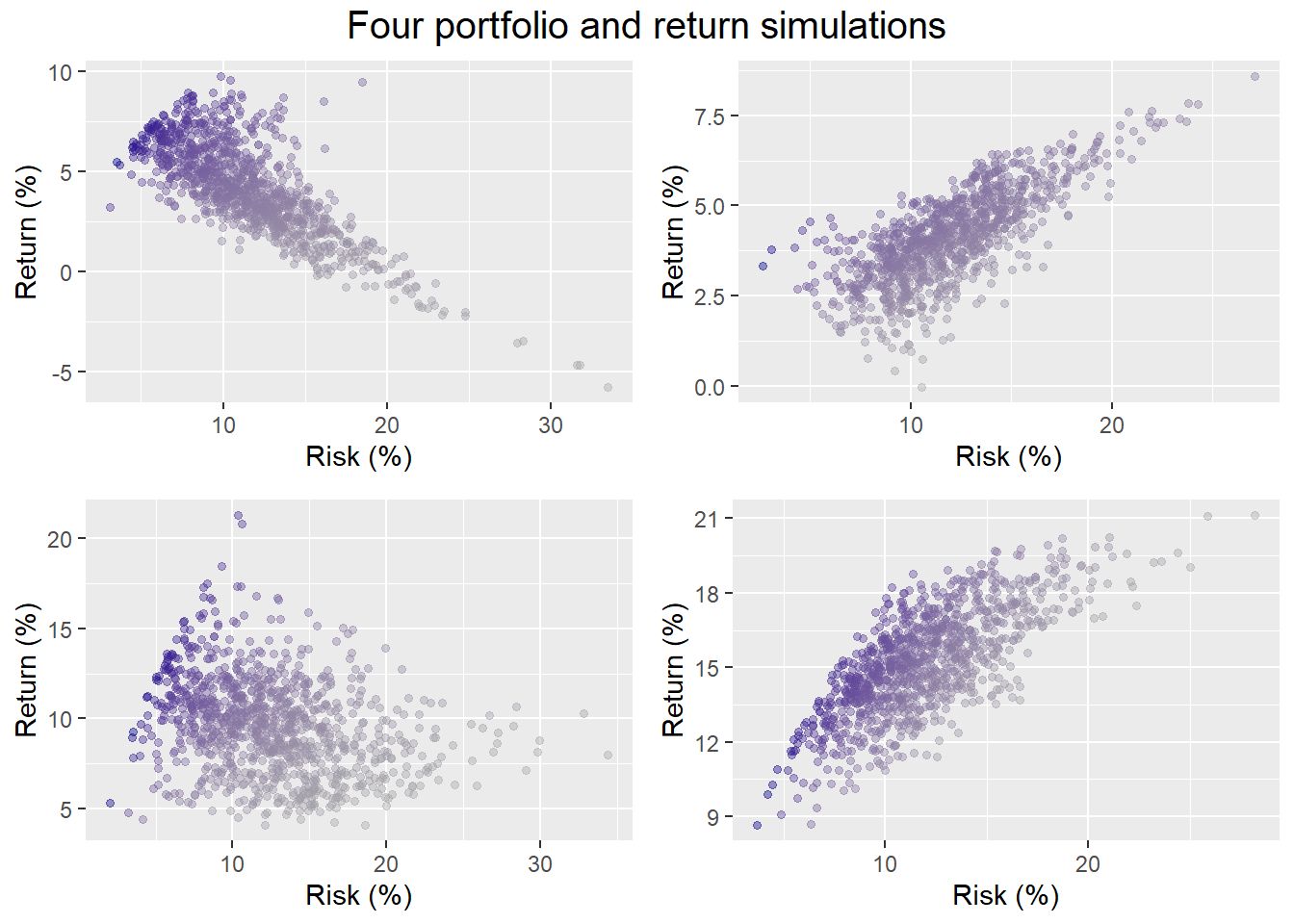

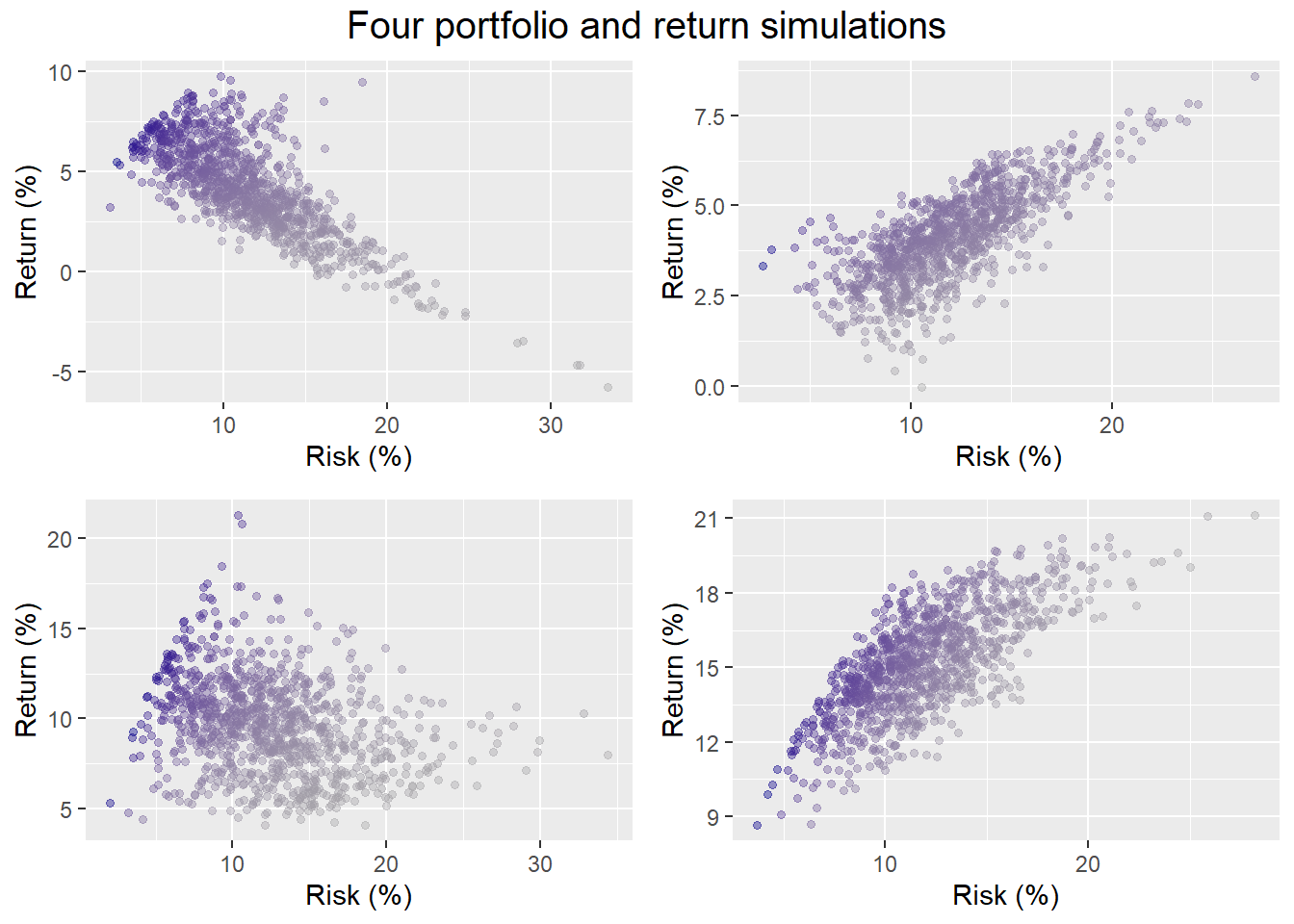

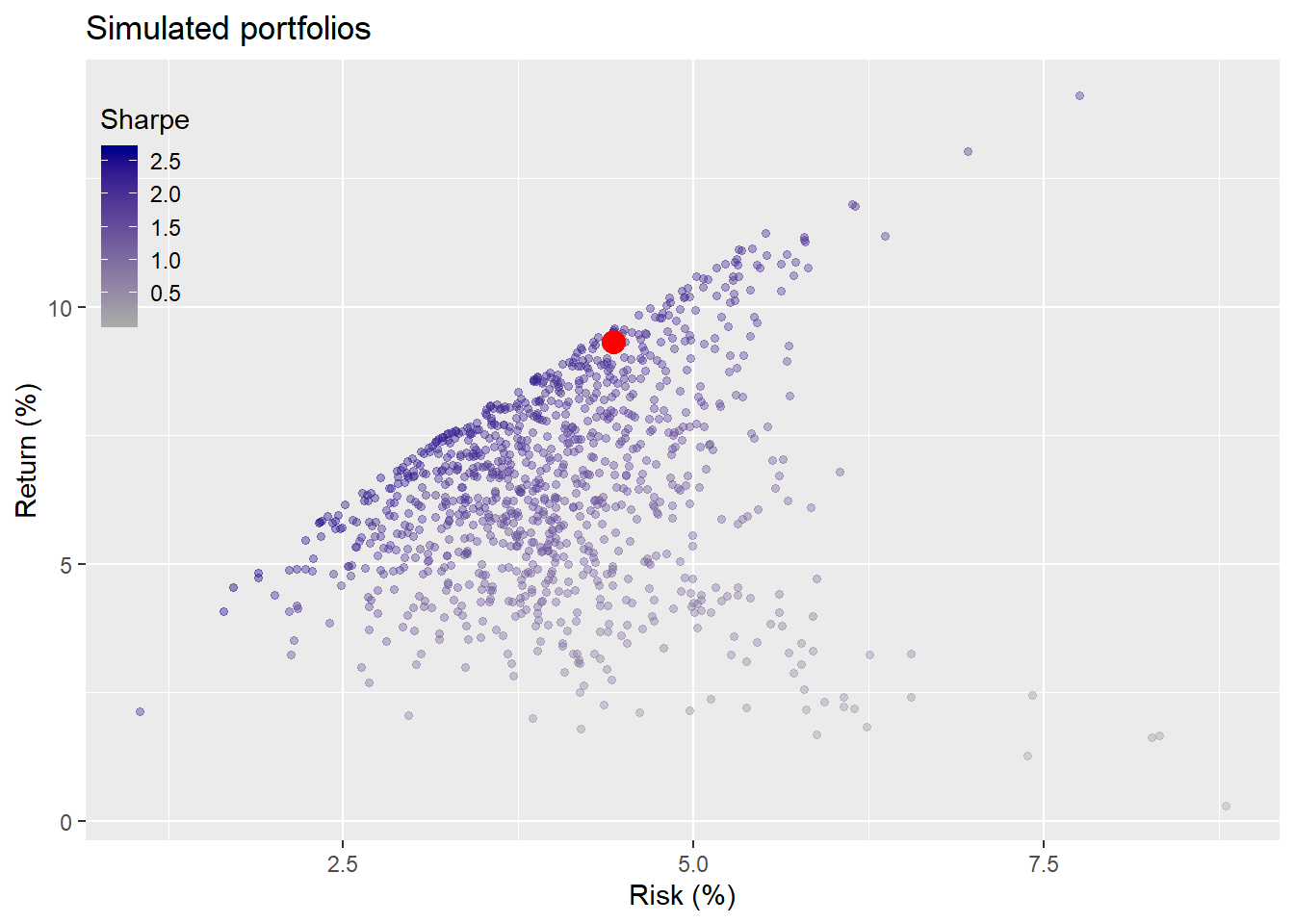

In our last post, we explored mean-variance optimization (MVO) and finally reached the efficient frontier. In the process, we found that different return estimates yielded different frontiers both retrospectively and prospectively. We also introduced the concept of satsificing, originally developed by Herbert Simon. Simply put, satisficing is choosing the best ...