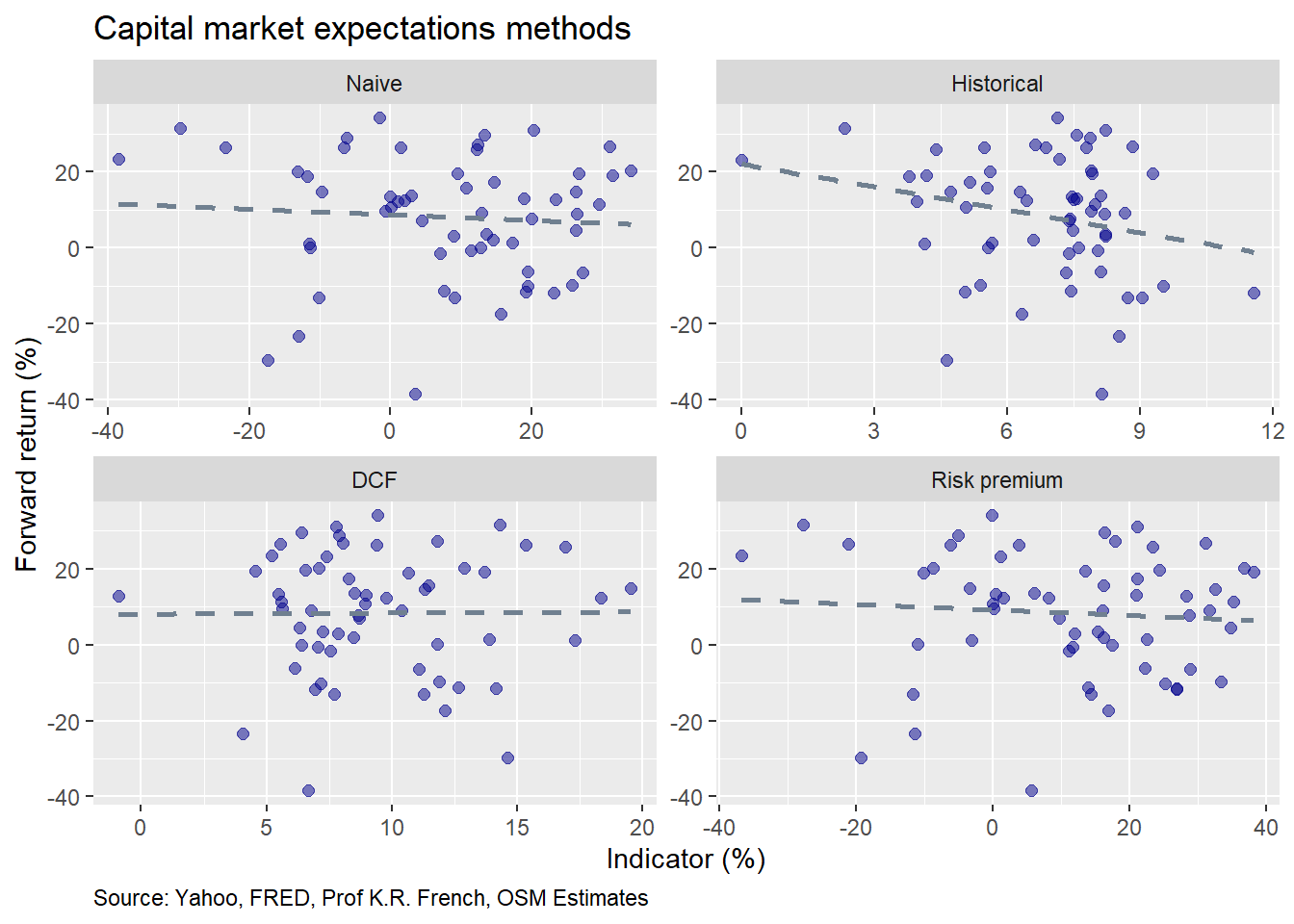

Testing expectations

In our last post, we analyzed the performance of our portfolio, built using the historical average method to set return expectations. We calculated return and risk contributions and examined changes in allocation weights due to asset performance. We...