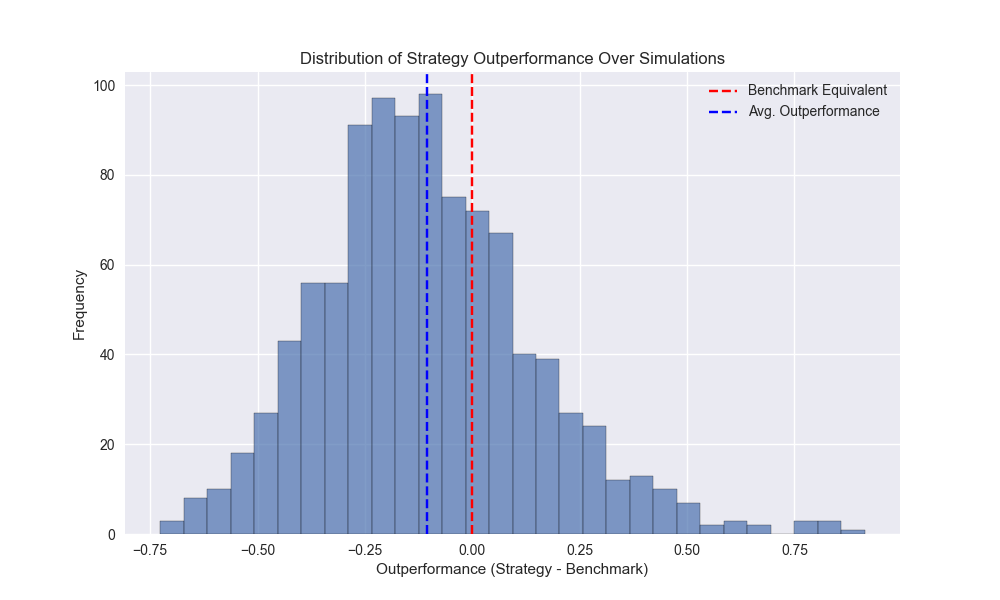

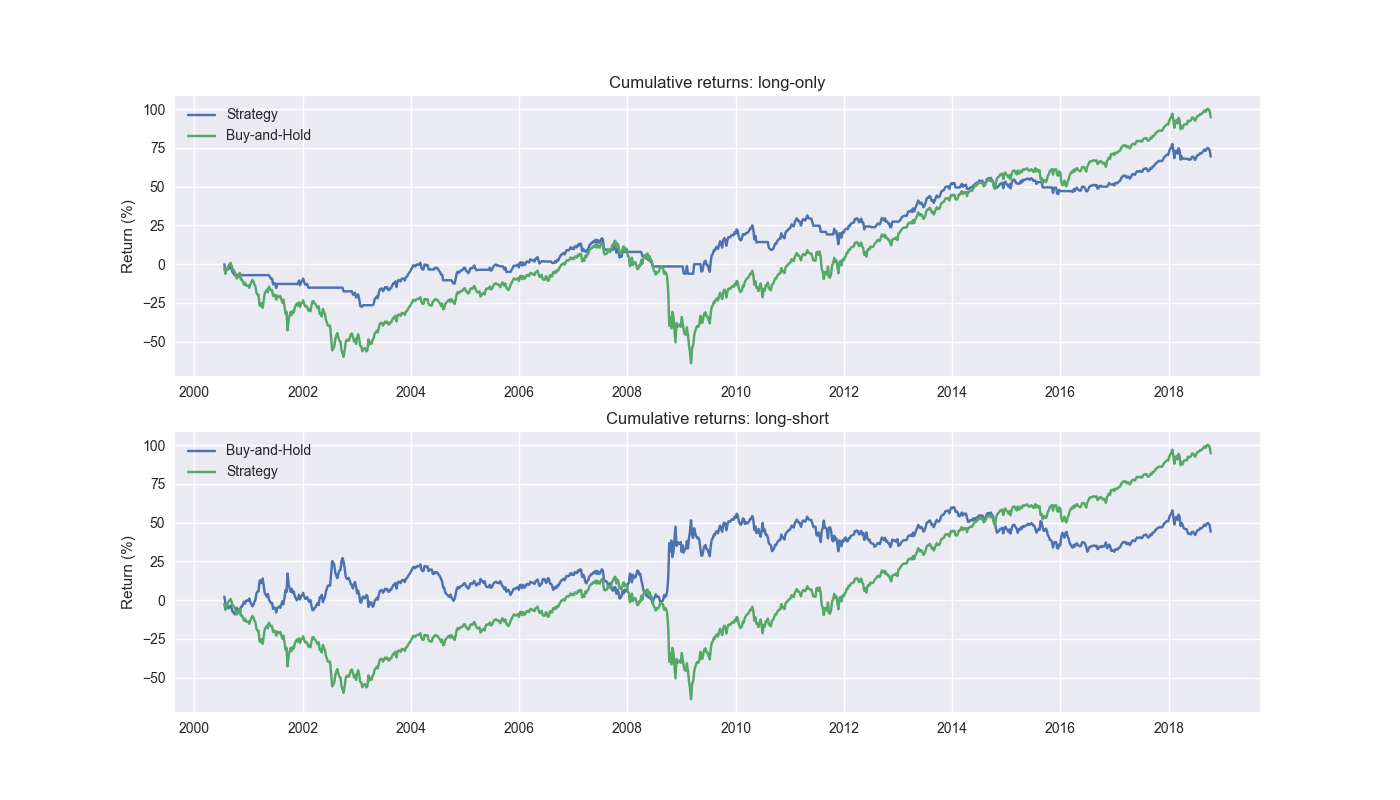

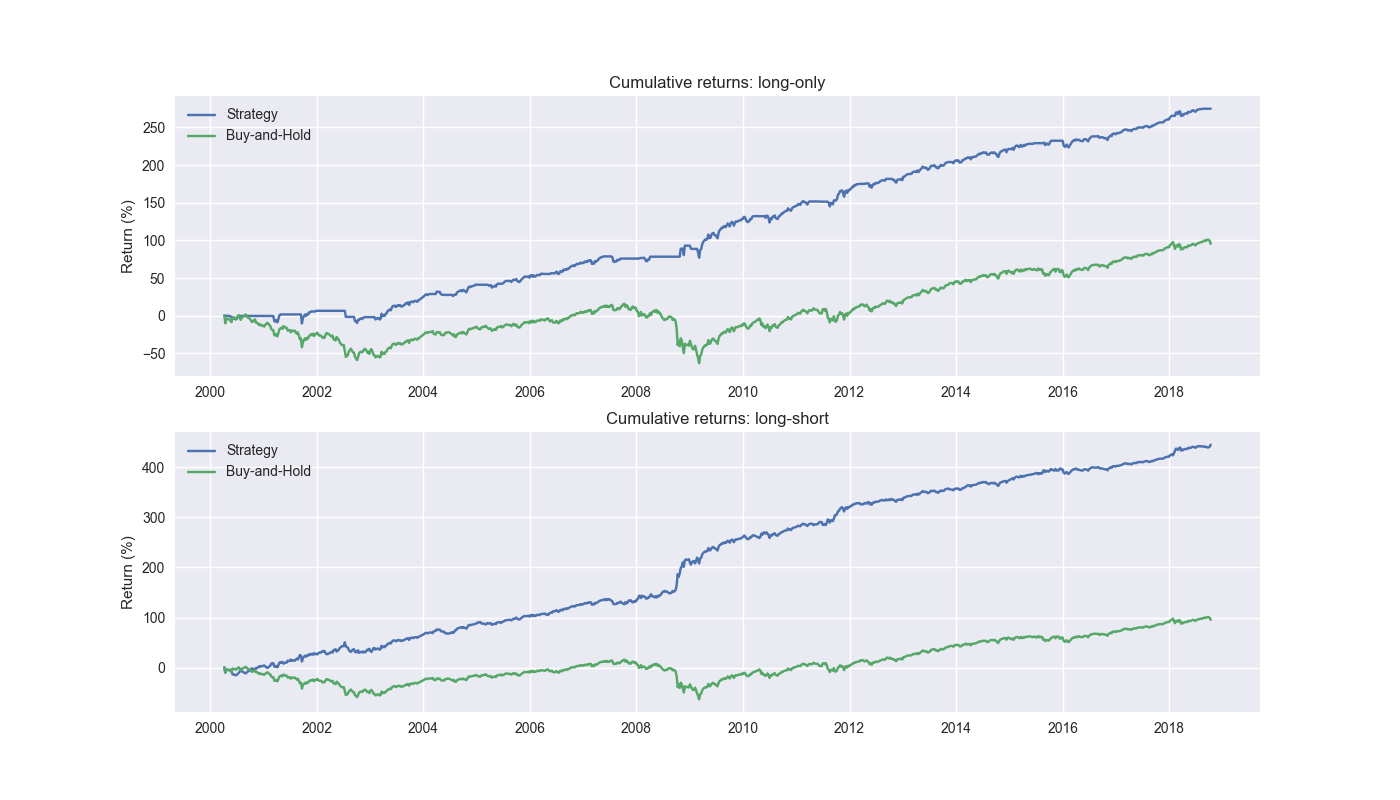

Day 20: Strategy Sample

On Day 19, we introduced circular block sampling and used it to test the likelihood the 200-day SMA strategy would outperform buy-and-hold over a five year period. We found that the 200-day outperformed buy-and-hold a little over 25% of the time acr...