Discounted expectations

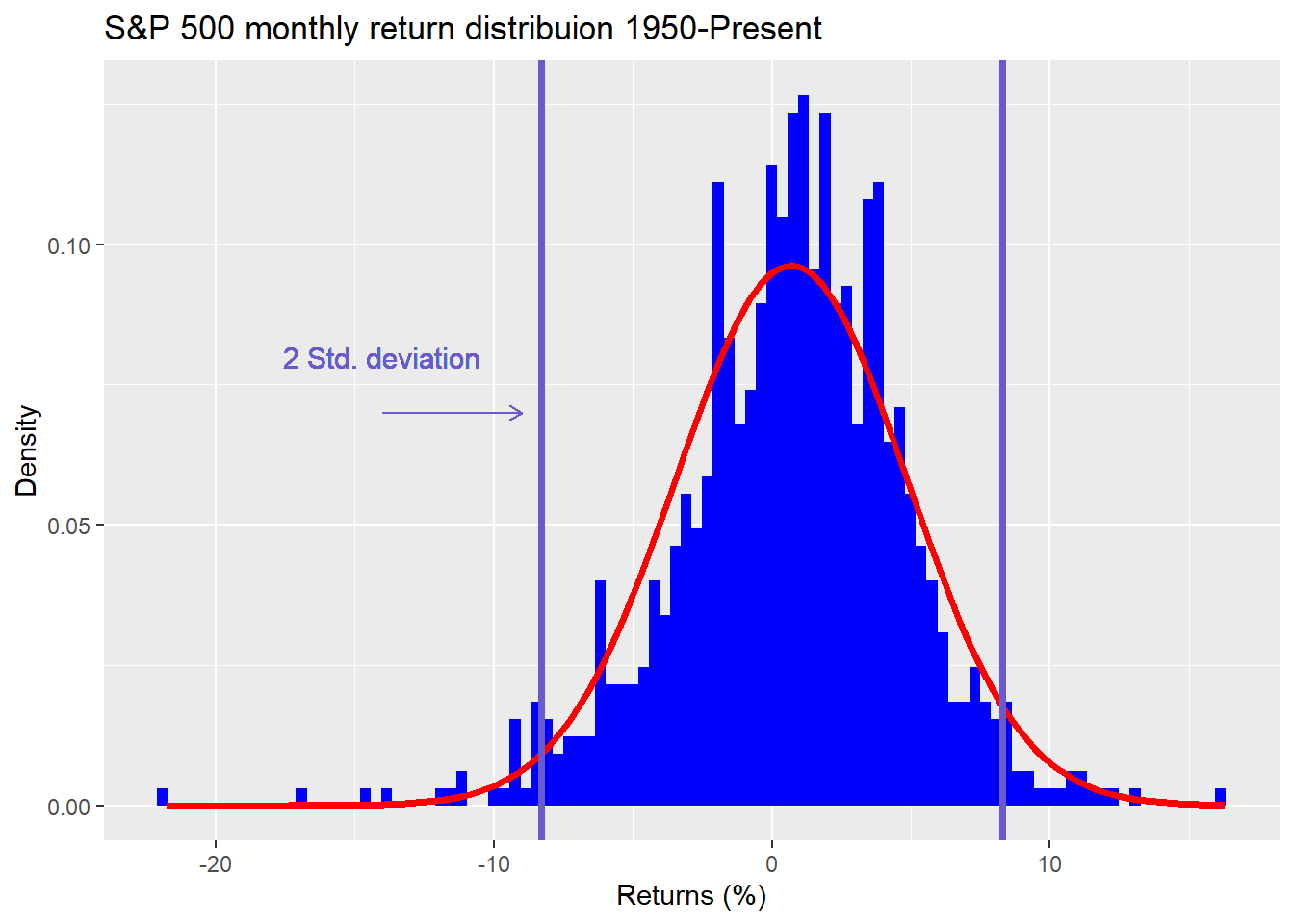

After our little detour into GARCHery, we’re back to discuss capital market expectations. In Mean expectations, we examined using the historical average return to set return expectations when constructing a portfolio. We noted hurdles to this approach due to factors like non-normal distributions, serial correlation, and ultra-wide confidence intervals.

...