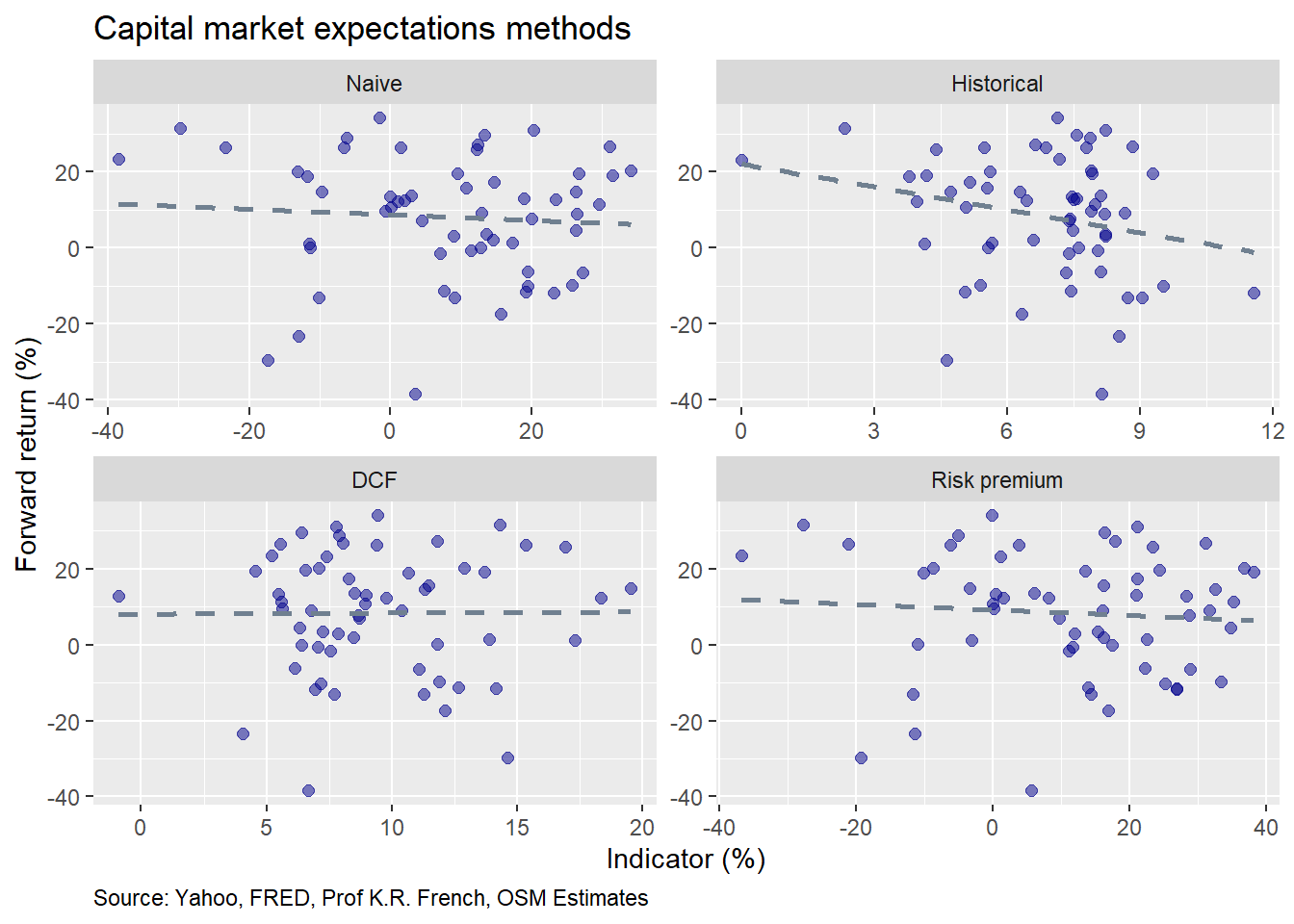

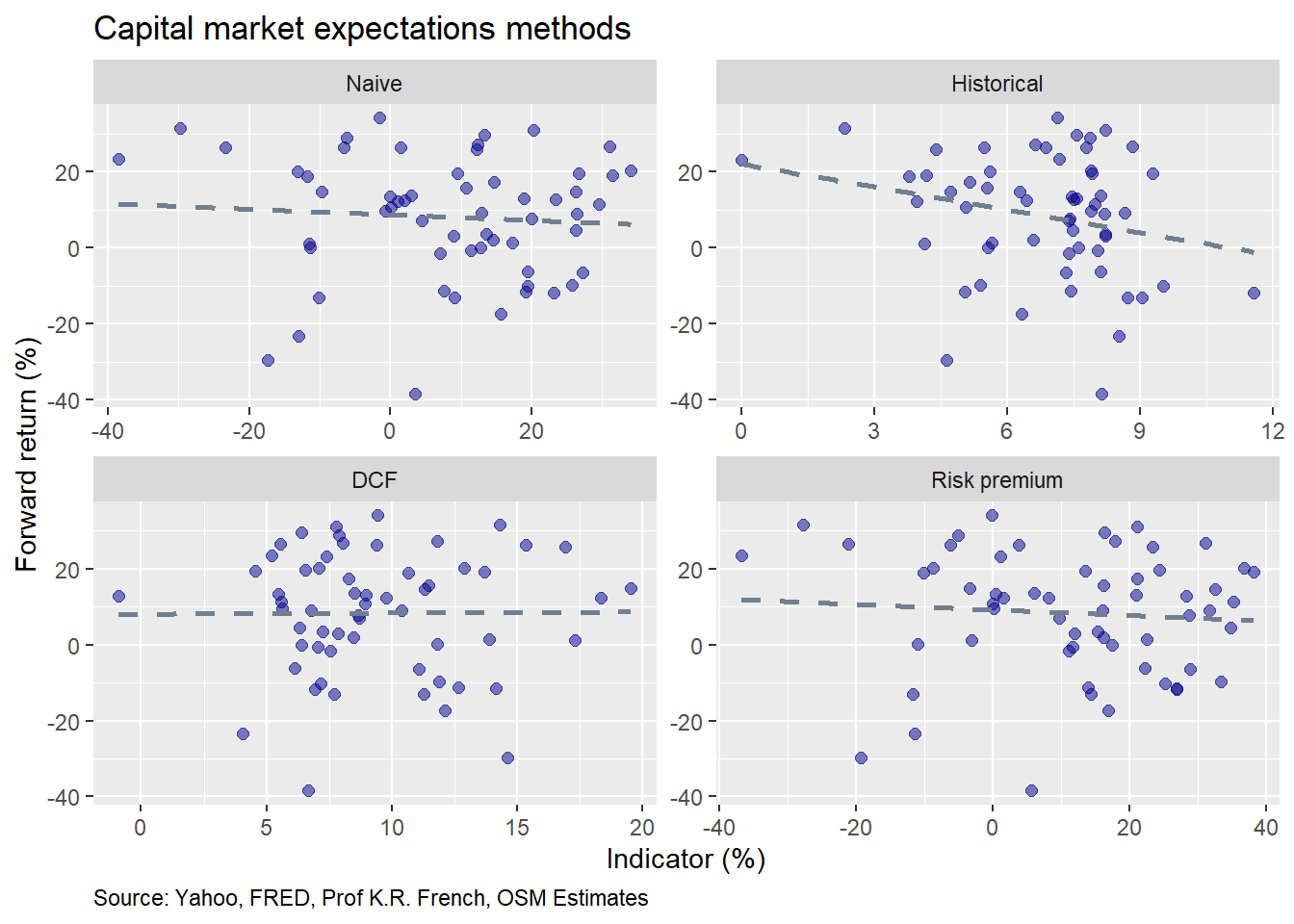

Mad methods

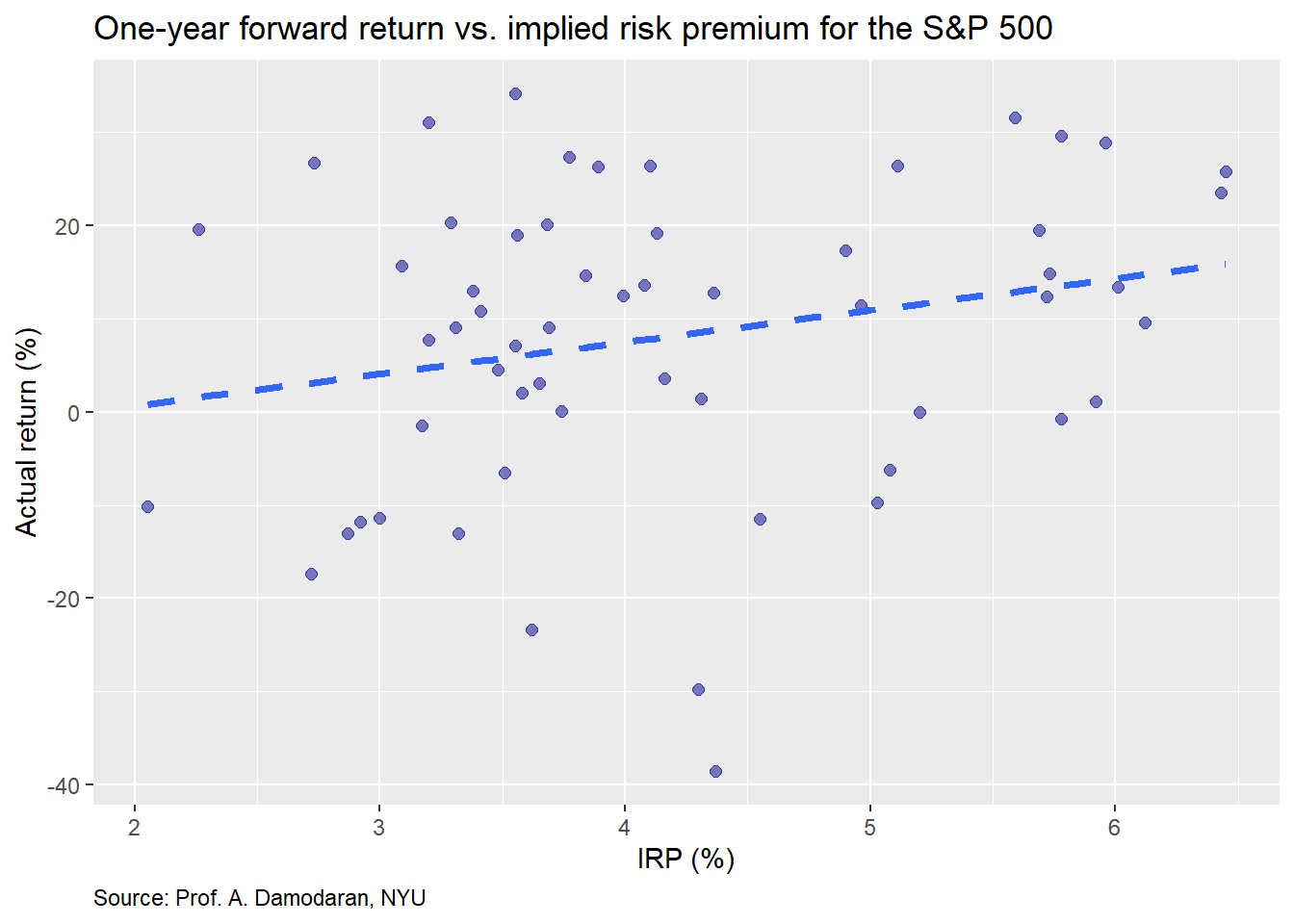

Over the past few weeks, we’ve examined the three major methods used to set return expectations as part of the portfolio allocation process. Those methods were historical averages, discounted cash flow models, and risk premia models. Today, we’ll bring all these models together to compare and contrast their ...