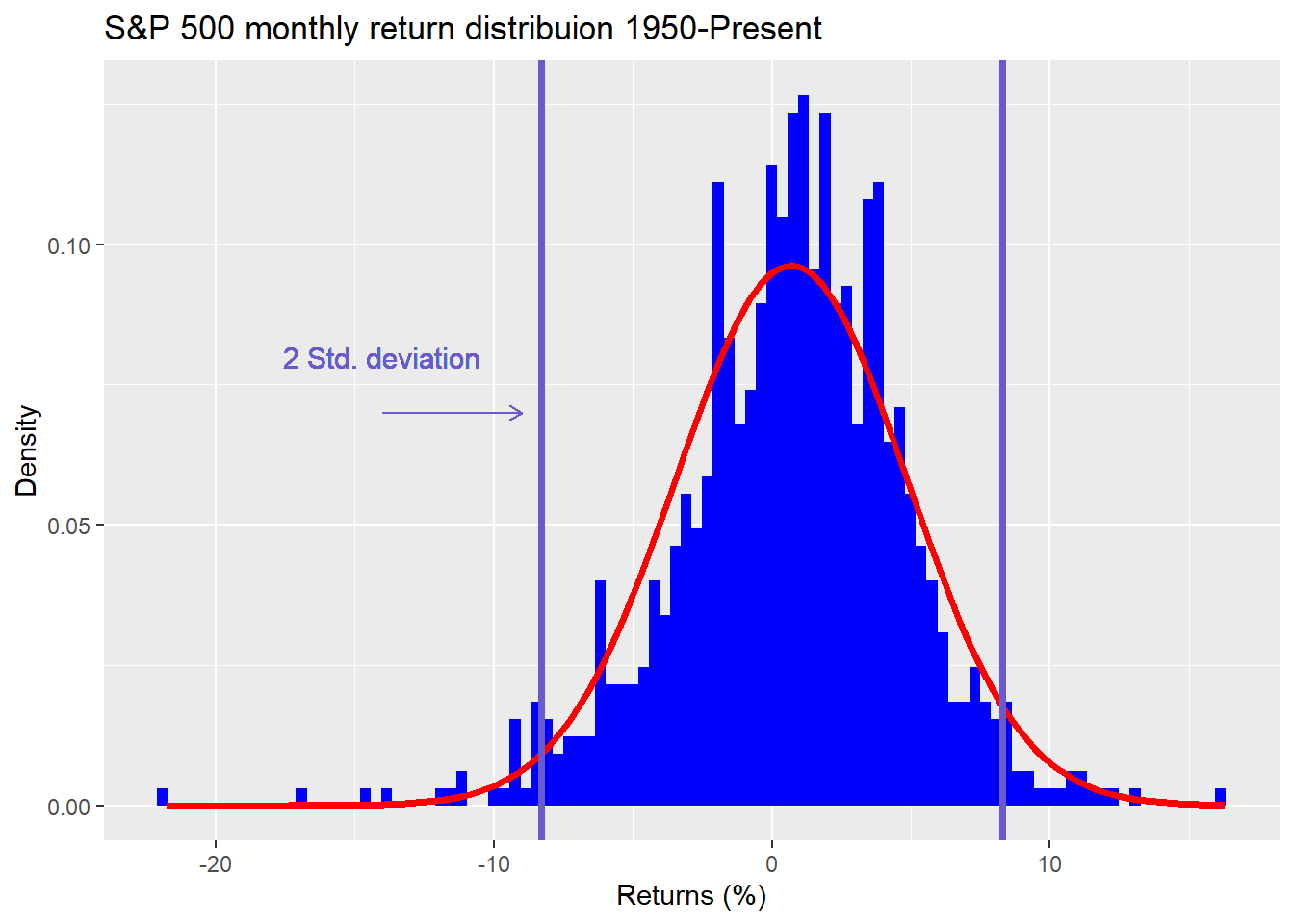

Mean expectations

We’re taking a break from our extended analysis of rebalancing to get back to the other salient parts of portfolio construction. We haven’t given up on the deep dive into the merits or drawbacks of rebalancing, but we feel we need to move the discus...